End of the Bull Market?

Emerging secular risk

"A good hockey player plays where the puck is. A great hockey player plays where the puck is going to be.” – Wayne Gretzky.

One of the longest bull markets of our lifetimes may be ending and many investors may not be prepared for what comes next.

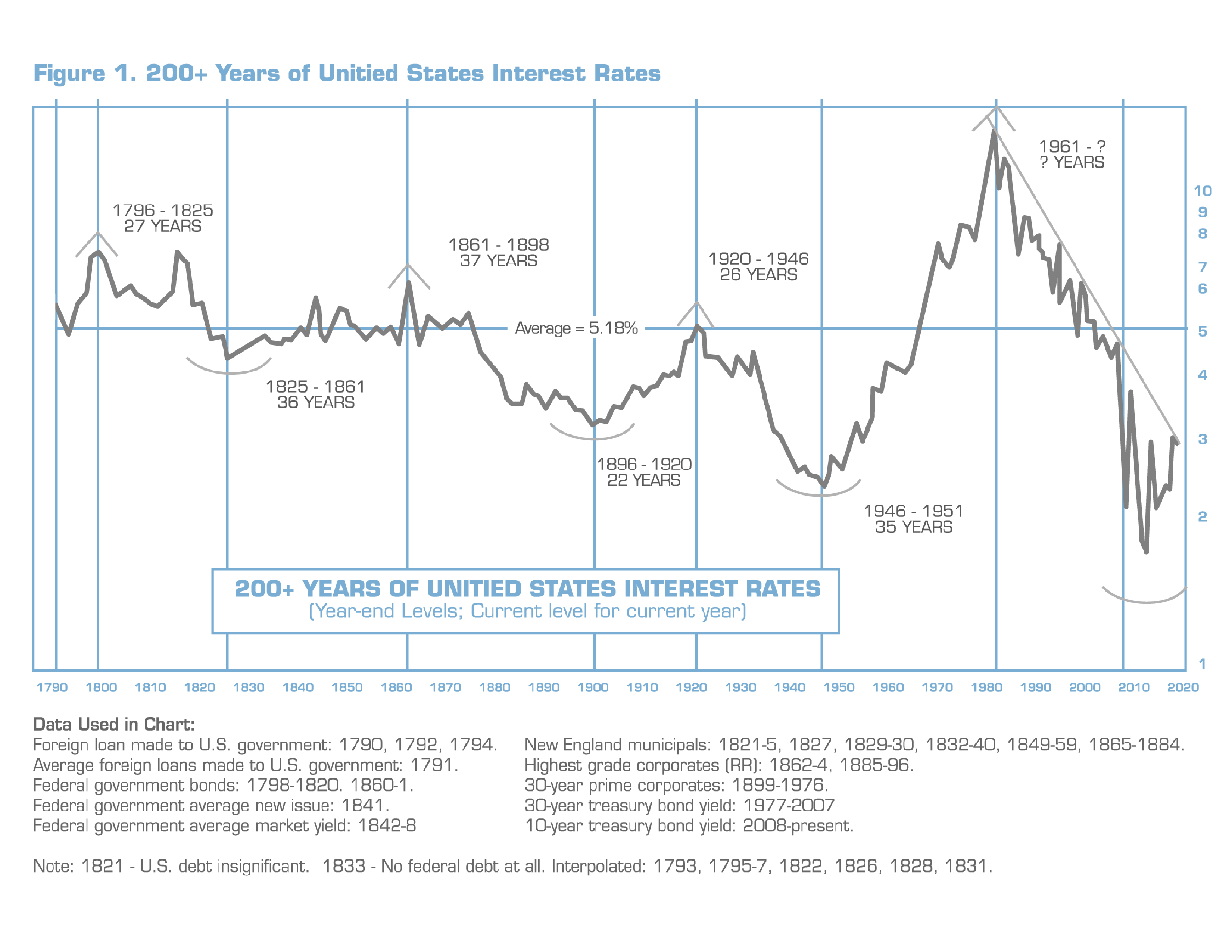

Surprisingly, we are not talking about the stock market but rather the bond market. Interest rates have been falling (and hence bond prices rising) for more than 35 years. That changed in 2018 and it may signal the start of a long period of higher interest rates. History demonstrates that interest rates often trade in 30+ year cycles (see chart below*), and we have reason to believe that they will climb for the next several decades. If you knew a 30-year bear market was starting, what would you do? Principal losses in excess of the annual bond income earned could become the norm. With over $22 Trillion in U.S. government debt, exploding pension burdens for municipalities and increasing levels of corporate and foreign debt, it is reasonable to believe investors may require higher interest rates in the future. Investors in mutual funds or exchange traded funds (ETF’s) are particularly exposed to this and numerous other risks.

* Chart Source: Louise Yamada Technical Research Advisors, LLC

If you buy a bond fund at a unit price of $10, what will it be worth when you sell? Unfortunately, you do not know. The fund may be paying annual income of 2% but if the price falls to just $9 per unit, the principal loss has just eroded 5 years of interest payments. Since interest rates have been falling for such a long time, today’s investors have only known stable or increasing unit prices. Mutual fund managers are often forced to buy or sell bonds based on the inflows and outflows of other investors into their funds, not based on your specific investment objectives. Outflows could potentially accelerate should interest rates continue to climb and bond fund values fall. This could result in increased transaction costs and taxes. Some fixed income mutual funds charge redemption fees if you sell prior a specified time frame.

At Premier, we recommend owning individual bonds as opposed to bond funds or ETFs. When you purchase an individual bond, you receive your principal back at maturity. If you buy a $100,000 5-year, government guaranteed, US Treasury bond at par, you will receive your $100,000 back in 5 years regardless of what happens to interest rates. The redemption price of a bond fund in 5 years will depend on the then-current level of interest rates and credit quality of that fund portfolio at that future date, which cannot be known at the time of purchase.

There are numerous other benefits to purchasing individual bonds: certainty of principal repayment and credit quality, customization of income and tax payments, and transparency. Unlike a bond fund, a skilled portfolio manager buying individual bonds can customize the portfolio to meet specific income needs instead of the needs of a fund’s supposed “average investor”. A managed portfolio of individual bonds is highly transparent. You can see and control the bonds you actually own, review their quality and understand the principal values you will receive at maturity. Do you know the type of bonds (quality ratings, insurance, backing etc.) that are held in your bond fund? With an individual bond portfolio, your portfolio manager can realize or defer tax gains or losses based on your specific tax situation. Mutual fund investors must accept whatever gain or loss the mutual fund throws off. Investors may even owe taxes on gains in which they did not participate. There may also be income tax benefits to investing in individual bonds. A Treasury bond might be exempt from your state income taxes, which is increasingly important given the reduction in state and local income tax deductions. Are you better off with more or less tax-exempt income? Post tax reform, many investors now benefit from a combination of both taxable and tax-exempt bonds to optimize their tax situation which can be accomplished using individual bonds.

Do you know what you are paying your mutual fund manager? You might think this less risky and customized service costs more than your mutual fund fees. This is not likely the case. Premier has very competitive pricing on fixed income management services. With the rare and undesirable combination of low yields and rising risks to your investment principal…. Is your portfolio positioned for the future or is it living in the past?

Joseph T. Seminetta

Thomas Grooms, CFA

Premier Asset Management LLC

PremierAssetManagement.com

Premier Asset Management LLC is a wholly owned subsidiary of Old National Bancorp, Inc, a publicly traded regional bank holding company (NASDAQ Global Select Ticker: FMBI). Our partnership enables Premier Asset Management LLC to focus on managing client portfolios and providing exceptional service. Other tasks are outsourced to specialists at Old National. Premier Asset Management LLC is not FDIC insured. Investments are not deposits or obligations of the institution and are not guaranteed by the bank. Investments are subject to investment risks, including possible loss of principal. Information provided is obtained from sources deemed to be reliable; but is not represented as complete, and its accuracy is not guaranteed. The information and opinions given are subject to change at any time, based on market and other conditions, and are not recommendations of or solicitations to buy or sell any security. Opinions and forecasts expressed herein may not actually occur.