What Does Your Ag Lender Look For?

How to position your farm for success in today’s agricultural economy

Farmers face many difficult financial questions. What’s the best way to access enough working capital to get through the season? Is it a good idea to rent adjacent acreage that becomes available? What’s the return on investment for a new piece of equipment? How will the farm be transitioned to the next generation?

These complex questions require a comprehensive and ongoing analysis of the farm’s finances. A trusted banking advisor who understands the agricultural marketplace can help farmers navigate the financial decision making process to help them reach their goals.

One of the best ways to create a productive relationship with a lender is to know what they’re looking for. Lenders want to understand your financial situation now and your plans in the years to come.

"We want our clients to farm well into the future, so we want to work closely with them through all stages of their business,” says Rebecca King, Head of Agriculture at First Midwest Bank. “That’s our passion.”

Farmers adapt to a changing business

Farming has never been more important. The world’s population is expected to reach 9.1 billion people in 2050, up from 7.7 billion in 2018. It’s estimated that farmers must increase food production by 70 percent from 2007 levels to meet the needs of a larger population.

As food demands grow, the business of farming is changing rapidly. New technology is making it easier

to manage a farm and use data to make critical business and agronomic decisions to reduce risk. At the same time, farmers need a trusted lender to finance their changing operations.

First Midwest Bank is now collaborating with Granular, the leading provider of farm management software to provide Midwest farms with increased access to capital and technology.

First Midwest Bank has approximately $17 billion in assets and is the #1 U.S. based agricultural bank in Illinois*. The bank is headquartered in Chicago, but its roots are in the local communities it serves. First Midwest has 10 dedicated ag loan officers located in Northern, Western and Central Illinois who work with more than 400 farms across Illinois, Indiana and Iowa.

“Granular and First Midwest Bank customers have a shared commitment and vision that better technology on the farm will strengthen the financial health and risk management of their businesses,” says King. “This is more crucial than ever in the current ag economy.”

Macro trends impact agricultural lending

Today’s financial environment is affected by several factors:

Low relative debt. U.S. farm assets in 2017 totaled more than $3 trillion and the level of equity in farms is strong. Equity is concentrated in real estate. The total debt-to-equity ratio in 2017 was 14.5%, though this number can vary. Small farms tend to have higher levels of equity. Large farms looking to grow tend to have a higher

debt-to-equity ratio, sometimes as much as 35%.

Age. The average age of a farmer is 58 years old. Granular predicts that the generational transfer of farms may take place at a more frequent rate in the next five years. The use of technology may increase with the transfer of farms to younger generations. Bankers consider retirement in the evaluation of a farm’s finances. The older generation may plan to retain quite a bit of equity in the land and collect cash rent as a way to finance retirement. That equity is not making the transition to the younger generation which means that the farm is not as well capitalized going forward. “The new generation has to build equity through consistent profitability,” says King. “The focus is on cash and profitability and finding ways to maximize that.”

Working capital. More farms are challenged with shrinking working capital. This is important because it is the key metric used to evaluate the financial health of a farm and to finance cash flow from year to year. Working capital ratios — current assets divided by current liabilities — have been falling. The sector is going into its 4th year of commodity prices that are not returning significant profitability to the farmer. As a result, working capital may be zero or even negative. First Midwest typically looks for a working capital ratio of 1.2 x or more. “Farmers need to evaluate what they can do to improve their working capital position in order to move forward,” says King. “Farmers need to watch their costs, so they can keep the working capital ratio where it needs to be and improve profitability when the opportunity arises.” Also, farmers that anticipate growth need to maintain a healthy working capital ratio in order to have access to long-term capital.

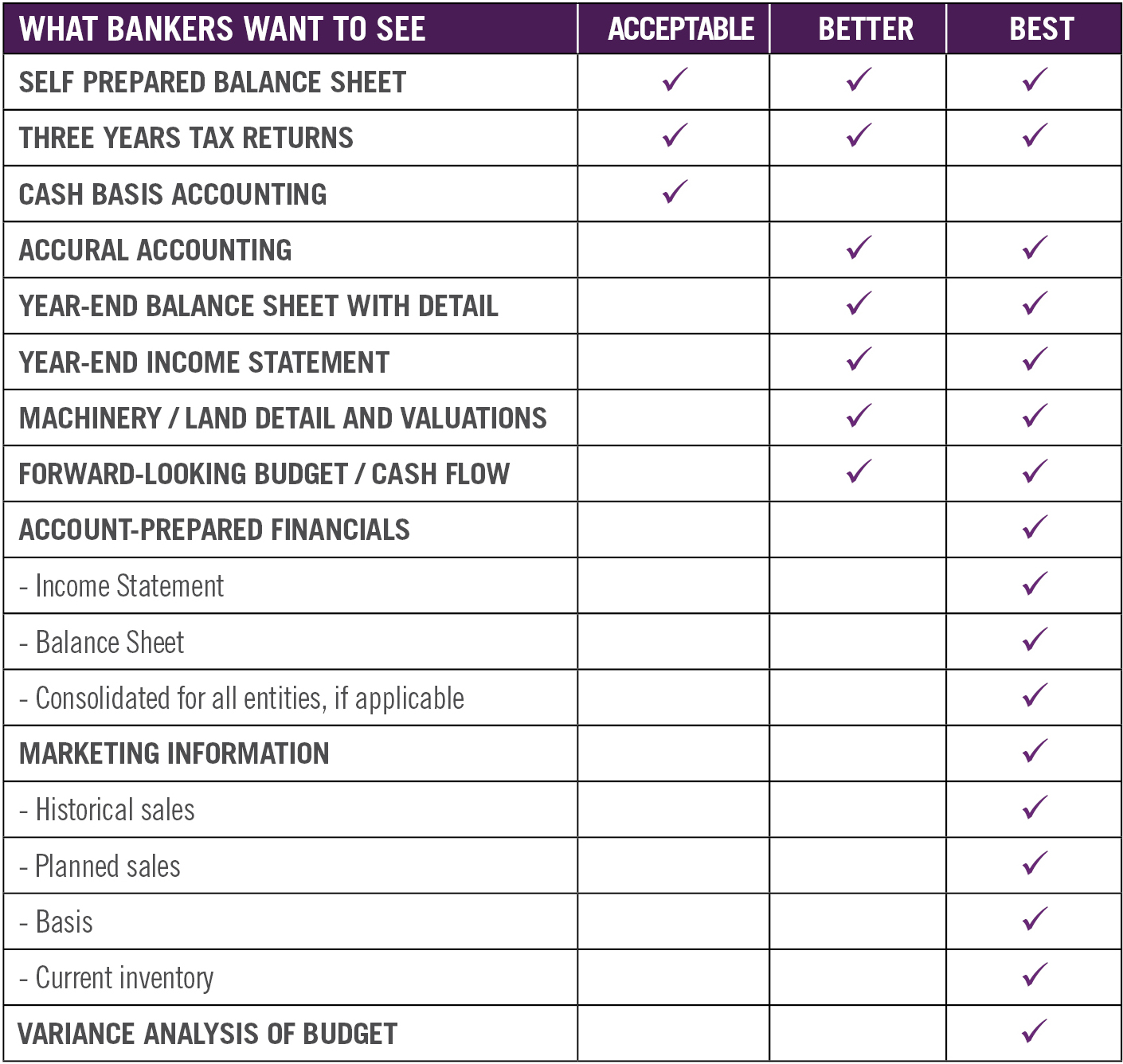

Keep Robust Records

Lending decisions depend on the performance and metrics of an individual farm. The first step toward loan approval starts with robust financial records that demonstrate a farm’s sufficient capacity to repay current and proposed debt.

Records typically fall into three categories: acceptable, better and best. Here’s what each includes:

Acceptable records. A self-prepared cash basis balance sheet and three years of tax returns.

Better records. A better approach is to provide a Farm Business Farm Management style record using the accrual basis of accounting.

Why is that important? A tax return on a cash basis does not really show the farm’s actual profitability. It may help the farmer save on taxes and provide more cash flow, but it does not give the banker the best picture of how the farm is actually performing, says King. The accrual method of accounting demonstrates the changes in profitability between different crop years.

Good records include a year-end balance sheet with detail and a year-end income statement. The records show number of acres and debt per parcel. Machinery valuations are included, along with a forward-looking budget and estimated cash flows. “We want to have a good feel for the total net worth of the farm and the total available collateral,” says King.

Best records: The best records include the components of the first two categories plus statements that are prepared by an accountant with audited statements for all records. Also included is marketing information: historical and planned sales; and current inventory, plus a variance analysis of the budget. “When we have that information, it is much easier to understand what’s going on with the farm and to be of value to the farmer in the future,” says King. “We encourage our clients to have robust records.”

Detailed financial records have other benefits. While interest rates vary from client to client, financial records that provide a clear picture of the farm’s financial situation will be a benefit to your banking relationship which could translate into favorable interest rates and terms.

How and when does the farmer prepare this information?

First Midwest typically meets with farm clients after harvest in December or January. Farmers present their records as well as costs and pricing though these metrics can change from year to year depending on weather, market expectations and other factors.

First Midwest prefers to meet quarterly with clients for a real time profitability update. It provides an opportunity to compare projections with the actual outcome. A meeting also gives the farmer the opportunity to make adjustments and improve profitability, and to possibly secure an increase in working capital.

Granular Farm Management Software provides real time information that can be presented at the quarterly meeting. To make record keeping simple, Granular has a mobile app available to easily log information from the field.

After a plan and budget is developed, the farm team reviews Granular reports, marketing positions, prepaid supplies, and other items.

During busy season when farmers are making their decisions, they don’t have to be at their desk to input new information into their budget. “The key is that the information is on the cloud,” says King.

“Contracts are linked to the Chicago Board of Trade and updated every 10 minutes. Granular dashboards show break even yields and prices for all crops. Granular software allows the farmer to focus on farming while making it easy to answer financial questions, such as breakevens,” says King.

Good information is especially critical when times are tough. Some advice: Plan ahead and run different scenarios. Understand your costs. Hoping for better pricing is not a plan. It’s important to understand the source of costs and profits in order to make better decisions throughout the year. Also, maintain more than a year of working capital and don’t over leverage. “Be mindful,” says King.

Do you have the right banker?

To understand your farming business, it is critical that your lender has deep roots in agriculture. You should ask any lender you are considering working with what kind of ag experience they have. The Ag Lending Team at First Midwest Bank all come from farm backgrounds or are actively farming themselves. “We are aware of the issues farmers are facing and what is happening in the marketplace,” says King.

A trusted banking advisor can also point out the pros and cons of a decision. For example, a farmer may consider whether to add 1,000 acres to his operation, or review the effect of a lost lease on cash flows.

First Midwest is able to provide an outside look at the impact on cash flow, equipment needs and variables the farmer might not have taken into account. “That’s where we can add value,” says King.

“We can sit down and see what that means to current debt load and the adjustments that need to be made to maintain profitability,” says King.

King stresses the importance of the relationship. And the need to trust that your information will remain private and secure. Farmers are all about their own business, but they don’t want other people to be about their business, she notes. “We get that.” First Midwest takes privacy seriously. “Internal discussions about individual farms only involve the people in our organization who need to make lending decisions for our clients,” says King.

Establishing a strong lending relationship provides comfort to a farm business, enabling the producer to focus on agronomy during the growing season. Providing your banker with the records and access they need will have long-term benefits. “We want to be our clients’ trusted advisor. Having good financial information is the first step to establishing that relationship,” says King.

Get Connected

Connect with an Ag Lender at First Midwest Bank to add momentum to your farm business.

Rebecca King

RebeccaKing@FirstMidwest.com

309-341-5007

Galesburg, IL

*Source: American Bankers Association.